My best-performing crypto position over the last six years isn’t a trade. It’s not a copy trader. It’s not a 100x altcoin call I made on Twitter. It’s an automated $100-a-week BTC buy I set up in 2020 and forgot about. I checked it last month and it had quietly compounded into something significantly larger than my “active” trading account.

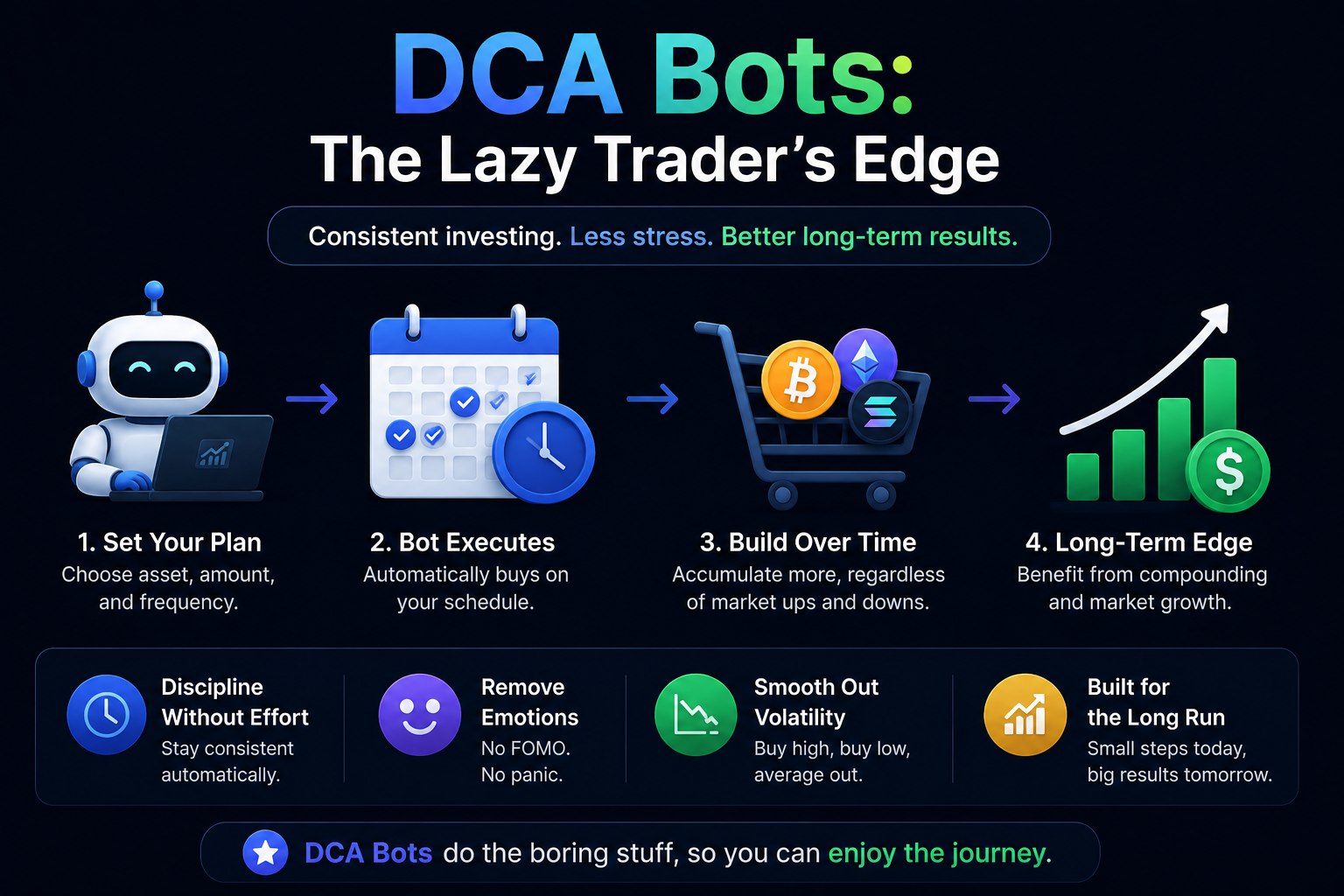

Welcome to dollar-cost averaging. It’s the dullest strategy in crypto. It’s also the one that beats most of you, most of the time, with no skill, no charts, and no late nights. DCA bots automate it so even the laziest version of you can’t mess it up. This post is how they work, why they work, and the exact settings I use on BitGet. Some links here are affiliate. I’ll flag them.

Short answer: A DCA bot buys a fixed amount of a chosen crypto on a fixed schedule, regardless of price. It removes the single biggest mistake retail traders make — trying to time the market — and accumulates a position at a respectable average price over time. Historically, DCA into BTC over any rolling 4-year window has produced positive returns, including windows that crossed the 2018 and 2022 collapses. Set one up, fund it, walk away.

Set up a DCA bot on BitGet → (affiliate)

Key takeaways

- DCA stands for dollar-cost averaging — buying a fixed amount on a fixed schedule.

- DCA bots automate the buys so emotion doesn’t enter the picture.

- The strategy works because it removes timing risk and forces buys during fear periods.

- For most retail traders, DCA outperforms attempts at timing the market over multi-year horizons.

- Best assets for DCA: BTC, ETH, and a small basket of top-10 majors. Not memecoins.

- Every buy is a separate taxable lot. Tax software handles the maths.

What DCA is in plain English

Dollar-cost averaging is the simplest investment strategy ever invented. You buy a fixed amount of an asset on a fixed schedule, regardless of price.

- $100 of BTC every Monday at 9am.

- $50 of ETH every Friday after work.

- $25 of SOL every other Tuesday.

That’s the whole strategy.

You don’t look at the chart. You don’t wait for the dip. You don’t try to call the top. You just buy. Some weeks you buy near the high. Some weeks you buy near the low. Over time the average works out to something reasonable, and the position grows.

Why it has a name

Because the alternative — lump-sum investing — requires you to pick a time to deploy your capital. Picking a time is hard. Most people pick badly. They wait for “a better price” that never comes, or they pile in at the top because everyone on Twitter is happy.

DCA solves this by removing the decision entirely. You’re not picking entries. You’re spreading them.

A picture is worth a thousand words

Imagine BTC went from $80,000 to $60,000 to $100,000 over 12 weeks. If you’d dropped a lump sum at $80,000 at week one, you’d be up roughly 25% by week 12. Not bad.

If you’d DCA’d $1,000 a week instead, you’d have bought some at $80,000, some at $60,000 (the dip), and some at $100,000. Your average entry is around $75,000 and you’re up roughly 33% by week 12. The DCA outperformed because it forced you to buy more units during the dip without you having to be brave or smart.

That’s the whole edge. You don’t have to call the bottom. You just have to be there.

Investopedia’s definition of DCA covers the textbook version. The textbook is right.

Why DCA beats lump-sum for most retail

There’s an academic debate about whether DCA or lump-sum produces better returns. The maths says lump-sum wins in roughly two-thirds of historical scenarios because markets trend upward over long periods and earlier deployment captures more growth.

That’s true. It also misses the point for retail.

Retail doesn’t lump-sum well

For lump-sum to beat DCA, you need three things:

- The capital available all at once.

- The discipline to deploy it without flinching.

- The psychological tolerance to hold through a 30% drawdown the next month.

Almost no retail trader has all three. You don’t have $50,000 lying around in cash — you have a paycheque. You don’t have the discipline to deploy it the day before a flash crash. And if you do, you don’t have the stomach to hold through it.

DCA solves all three. The capital comes in monthly anyway. You don’t have to be brave. You don’t have to be smart. You just have to set up the bot once.

The data on BTC

Pull any 4-year rolling window of BTC price and DCA $100 a week. Every window since 2014 has produced a positive return at the end. Every single one, including windows that crossed the 2018 bear market and the 2022 collapse.

You can check this yourself with CoinGecko’s BTC historical data and a spreadsheet. The strategy is so consistent across history that it borders on boring. Which is exactly why it works.

What lump-sum gets right (and DCA gets wrong)

Lump-sum wins in steadily rising markets where the capital deployed early captures more growth. If you’d lump-summed at the bottom of every cycle, you’d outperform DCA. The problem: you can’t identify the bottom in real time. Everyone says they would have bought BTC at $4,000 in 2018. Almost nobody did.

DCA is the strategy that protects you from your own bad timing. The cost is some upside in raging bull markets. The benefit is you actually execute the strategy instead of waiting for “a better entry” forever.

The behavioural advantage

This is the part most analyses skip, and it’s the part that actually matters.

You will not buy the dip

It’s 4am. BTC just dropped 18%. Twitter is on fire with “this is the end” posts. Your portfolio is bleeding red. The rational move is to buy. The actual move is to not buy, because you’re scared.

A DCA bot does not get scared. It executes the buy on schedule. The bot bought your best entries in 2020. The bot bought your best entries in 2022. The bot will buy your best entries in the next collapse, while you’re sitting on the sidelines telling yourself you’ll wait for “a better price”.

You will not sell the top

Inverse problem. The bot doesn’t try to call the top. It just keeps accumulating until you tell it to stop. The number of retail traders who held through 2020’s run only to dump everything at the bottom of 2022 because they “needed to lock in profit before it all goes to zero” is in the millions.

DCA bots remove the need to call the top. You decide separately, with a clear head, when to take profit.

You stop watching the chart

The single biggest hidden cost of active trading is the time you spend looking at the chart. Every hour you spend on TradingView is an hour you didn’t spend earning more fiat, building a business, or learning something useful.

A DCA bot lets you not look. The trades happen. You check in monthly. The rest of the time you live a life.

If you want the structured version of the behavioural side of trading, the community I learn from is Trade Travel Chill (affiliate). It’s the one place I’ve found that talks honestly about the psychology piece without selling a course.

DCA bots vs manual DCA

You can do DCA without a bot. You just buy $100 of BTC every Monday yourself.

This works for about three weeks. Then:

- You forget one week.

- The market is red and you “wait until it stabilises”.

- You’re on holiday and the buy doesn’t happen.

- You’re feeling rich and you double the amount this week, throwing off the strategy.

Manual DCA dies of a thousand small exceptions. The whole point of DCA is that it removes decision-making. The moment you reintroduce decisions, you reintroduce all the same bad instincts that drove you to bots in the first place.

A bot doesn’t forget. A bot doesn’t wait. A bot doesn’t have feelings. It buys.

The DCA bot does three things manual DCA can’t

- Executes regardless of emotion. No skipping the buy on a red day.

- Executes regardless of presence. You can be asleep, on holiday, or unconscious.

- Tracks everything. Every buy logged with date, price, amount. Your tax export is one click instead of three months of spreadsheet work.

The marginal cost is roughly zero on most exchanges. BitGet’s DCA bot is free to use. Worth using.

BitGet DCA bot setup

The BitGet DCA bot lives under Trading Bots → Spot DCA. Here’s the actual setup.

Step 1: Pick the pair

Open the DCA bot. Search for BTC/USDT (or ETH/USDT, or whatever your chosen pair is). Confirm the pair.

Step 2: Set the schedule

Three options on BitGet:

- Daily: every X days.

- Weekly: every Monday/Tuesday/etc. at a chosen time.

- Monthly: on the same date each month.

For most people, weekly is the right answer. More on that in the next section.

Step 3: Set the amount

The minimum on BitGet is around $10 per buy. The realistic starting amount is $25–$100 per week, depending on your monthly capacity to deploy.

Rule of thumb: pick an amount you can sustain for 12 months without thinking about it. Sustainability beats size.

Step 4: Set the duration

You can set the bot to run for a fixed number of buys (24 weekly buys = 6 months) or run indefinitely until you stop it. I run mine indefinitely and review every 6 months.

Step 5: Fund and deploy

Make sure your USDT balance covers at least the first 4 weeks of buys. Click deploy. The bot is live.

That’s the whole setup. Five minutes. The detailed walkthrough with screenshots will go in the dedicated BitGet DCA Bot post when it’s published. For the broader bot suite, the crypto trading bots guide covers everything.

Topping up

If you can’t fund the bot for the full duration upfront, set a calendar reminder to top up monthly. Or set up an auto-deposit from your card. Either way, don’t let the bot run out — the moment a scheduled buy fails, you’ve broken the strategy.

Skip the setup — copy the bot directly.

The BTC accumulation bot I run is published on the BitGet bot marketplace. Two-click deployment.

Affiliate link. I may earn a commission at no extra cost to you.

How often to buy: daily vs weekly vs monthly

This is the question people argue about. Here’s the boring answer: it almost doesn’t matter.

Daily

Smoothest average price. More taxable events. Higher cumulative trading fees (though tiny per trade). Slightly better behavioural anchor because the bot fires often.

Good for: people with daily auto-deposits or who want maximum smoothing.

Weekly

The Goldilocks answer for most people. Fits with a typical pay cycle in many countries. Average price is close to daily DCA. Tax record is manageable. Fees are negligible.

This is what I run.

Monthly

Fewer trades. Larger position per buy. Tax record is cleaner. But you’re more exposed to bad timing on each individual buy — if your monthly buy lands on a local high, you’re stuck with that entry for the next month.

Good for: people who can only deploy capital monthly and want fewer trades.

The data on which wins

If you ran the maths on every rolling year of BTC since 2014, daily and weekly DCA produce essentially the same returns (within 0.5%). Monthly DCA shows slightly higher variance because each individual entry has more weight.

Pick the cadence that fits your life. The cadence is far less important than the consistency of execution.

Position sizing

This is where DCA bots become a real strategy, not a hobby.

The starting rule

DCA into crypto with no more than 10% of your monthly take-home pay. Some weeks you’ll want to do more. Don’t. The whole point is consistency at a sustainable level.

If your take-home is £3,000 a month, that’s £75 a week of DCA into BTC. Boring. Sustainable. That’s what works.

Adding pairs

Once you’ve run a single-pair DCA for 6 months and the rhythm is automatic, you can add a second pair. Common split:

- 70% BTC

- 25% ETH

- 5% one or two top-10 alts you have conviction on

I would not recommend a “diversified” DCA across 10 alts. The work of tracking them isn’t worth the marginal diversification benefit. Stick to BTC + ETH for 95% of the allocation.

When to scale up

If your income increases, scale the DCA amount proportionally. Don’t scale it because you’re feeling bullish. Don’t scale it because “the bottom is in”. Scale it because your sustainable monthly capacity changed.

If you suddenly have more capital available — bonus, inheritance, asset sale — lump-summing into BTC has worked historically. But many people do better psychologically by spreading it over 6–12 months of accelerated DCA. Either is fine.

DCA + grid combo

The strategy I actually run is DCA layered with a grid bot. Here’s how they fit together.

The roles

- DCA bot: long-term accumulation. Buys regardless of price. Builds the position.

- Grid bot: active capture of chop. Trades inside a range. Generates yield on already-held capital.

The DCA bot is feeding the long-term stack. The grid bot is squeezing extra return out of the active trading float.

The setup

- DCA bot: $100/week BTC/USDT spot, indefinite, set and forget.

- Grid bot: 5–10% of trading float on BTC/USDT spot grid, 50 grids, ±15% range, reviewed monthly.

The two don’t interfere. The DCA bot accumulates into the long-term hold. The grid bot trades the active float. Different pools, different goals, both running.

Together they cover both halves of the BTC strategy: passive accumulation and active capture. The whole rationale is in the grid trading explained post.

Tax: every DCA buy is a taxable lot

This is the section nobody wants to read.

Every individual DCA buy creates a separate tax lot. A weekly DCA over 5 years gives you 260 separate lots, each with its own cost basis and acquisition date.

When you eventually sell, the disposal is calculated against those lots using a method that depends on your jurisdiction:

- US: FIFO by default; specific identification allowed.

- UK: the 30-day rule and the matching rules under HMRC guidance.

- Most EU: FIFO or weighted average, varies by country.

A bot doing weekly buys produces a manageable tax record. A bot doing daily buys produces 365 lots a year. Both are fine if you’re using crypto tax software.

What to do

- Export your DCA bot trade history from BitGet quarterly.

- Import to Koinly, CoinTracker, or CoinLedger.

- Let the software calculate the disposal maths when you eventually sell.

The software costs $50–$200 a year depending on volume. Worth it. Doing the maths manually on 260 tax lots is a route to mistakes and missed deductions.

Income reporting on the buys

A DCA buy itself is not a taxable event — it’s an acquisition. The taxable event comes when you sell, swap, or spend the asset. So the bot can run all year and you don’t owe any tax until you dispose.

This is one of the small structural advantages of DCA over actively trading the same capital. Active trading triggers tax on every closed trade. DCA defers tax until you take profit.

When DCA stops making sense

DCA isn’t unconditional. There are scenarios where the strategy breaks down.

When the asset’s long-term thesis is broken

DCA works because the asset is something you believe will appreciate over a multi-year horizon. If the underlying thesis breaks — the project’s team disappears, the token’s utility collapses, the chain halts — DCA into it is just a steady transfer of cash into a dying asset.

This is why DCA into memecoins is a terrible strategy. The thesis is “it pumps because it pumps”, which can stop being true overnight. DCA into BTC and ETH is fine because the long-term thesis (digital gold, programmable settlement layer) has held up across multiple cycles.

When you’re in a deep bear floor and need the cash

If you’re DCA’ing through a bear market and your living situation changes — job loss, medical bill, family crisis — pulling money from a DCA position at a 60% drawdown is a real problem. The defence is to only DCA money you don’t need access to for 4+ years.

The strategy assumes you can outlast the cycle. If you can’t, don’t DCA. Hold cash.

When you’ve accumulated “enough”

This is the question almost nobody plans for. At some point your BTC position becomes a meaningful percentage of your total wealth. Continuing to DCA into it makes the concentration worse, not better.

A reasonable rule: cap crypto at 10–25% of total net worth depending on age, risk tolerance, and other holdings. Once you hit the cap, stop DCA’ing more crypto. Redirect the savings to index funds, cash, or whatever else fits the portfolio. The passive income crypto post covers the yield-side complement to DCA accumulation.

DCA bots vs other accumulation strategies

Quick comparison of the options for buying crypto on a schedule.

| Strategy | Pros | Cons |

|---|---|---|

| Manual DCA | No platform lock-in, full control | Misses buys, emotional execution |

| DCA bot (exchange) | Automated, free, tax export | Tied to that exchange |

| Auto-invest on Revolut/Coinbase | Easy for beginners | Higher fees, fewer pairs |

| Recurring buys via card | Works without a balance | Card fees of 1–3% per buy |

| Lump-sum | Statistically wins over long horizons | Most retail can’t actually do it well |

The DCA bot on a major exchange is the right answer for most people. Lower fees than card-based recurring buys, more pairs than fiat-only apps, automated unlike manual DCA.

If you’re new to buying crypto at all, how to buy crypto and how to buy bitcoin are the starting points before deploying a bot.

Security: don’t lose what you accumulate

A DCA bot accumulates a position over years. The single biggest threat to that position isn’t the market — it’s losing access to the exchange or having your account compromised.

Two-factor on the exchange

Google Authenticator or Authy. Not SMS. SMS 2FA is the single weakest link in account security and is the entry vector for most exchange hacks at the retail level.

Don’t trade from public WiFi

Coffee shops, airports, hotels. Account takeovers happen on networks you don’t control. I use NordVPN (affiliate) on any device that touches my exchange account. It’s not a magic shield but it removes the easy attacks.

Move long-term holdings off the exchange

A DCA bot that’s been running for 2+ years has accumulated a meaningful position. Once a quarter, sweep the surplus to cold storage — a Ledger Nano X or similar hardware wallet. The exchange holds the trading float; the wallet holds the long-term stack.

The longer playbook is in the how to store crypto safely post.

Set up a DCA bot in 5 minutes.

BitGet’s DCA bot is free, native to the exchange, and handles BTC, ETH, and most majors. The hardest part is deciding the amount.

Affiliate link.

Frequently asked questions

What is a DCA bot?

A DCA bot automates dollar-cost averaging by buying a fixed amount of an asset on a fixed schedule, regardless of price. It removes the timing decision and forces consistent execution.

Does DCA actually work for Bitcoin?

Yes. Every rolling 4-year window of BTC price since 2014 has produced a positive return when DCA’d weekly. This includes windows that crossed the 2018 and 2022 collapses.

How often should I DCA into crypto?

Weekly is the right answer for most people. Daily produces marginally smoother averages with more tax events. Monthly produces cleaner records with slightly more entry variance. Pick the cadence that matches your income.

How much should I DCA into Bitcoin?

A sensible starting rule is no more than 10% of monthly take-home pay. Sustainability matters more than size. Most retail traders fail by being too aggressive early and running out of capital.

Is lump-sum better than DCA?

Mathematically, lump-sum wins in roughly two-thirds of historical windows because earlier deployment captures more growth. Behaviourally, almost no retail trader executes lump-sum well — DCA is the more reliable strategy for most people.

Can DCA bots run on autopilot forever?

Yes, but review every 6 months. Make sure the underlying thesis still holds, the bot is funded, and the allocation still fits your overall portfolio. Fully forgetting the bot is fine for accumulation but bad for portfolio management.

Do I pay tax on DCA buys?

Not on the buy itself — only on the disposal (sell, swap, spend). Each DCA buy creates a separate tax lot with its own cost basis. Use crypto tax software like Koinly or CoinTracker to handle the maths.

What’s the difference between a DCA bot and a grid bot?

A DCA bot only buys, on a schedule, regardless of price — it’s accumulation. A grid bot buys and sells inside a range — it’s active mean-reversion trading. They serve different purposes and can be run alongside each other.

Final word

A DCA bot isn’t a strategy that gets you on a Bloomberg cover. It’s the one that quietly outperforms most of the people on that cover over the long run.

Here’s what I actually do:

- BTC/USDT DCA on BitGet, weekly, set indefinitely.

- Smaller ETH/USDT DCA, weekly.

- Top-up the funding balance monthly.

- Sweep accumulated coins to cold storage quarterly.

- Don’t look at the chart between sweeps.

If I were starting again today, I’d skip everything else for the first 12 months and just run a single BTC DCA bot. The compounding starts slow. By year three you can’t believe you ever traded actively.

Right — over to you.

Related posts

- Crypto Trading Bots: What Actually Works

- Grid Trading Explained: Profit From Sideways Markets

- How to Buy Bitcoin

- How to Store Crypto Safely

- Passive Income in Crypto Without Getting Rugged

External references

- Investopedia — Dollar-cost averaging explained

- CoinGecko — Bitcoin historical price data

- BitGet — Trading bot documentation

- IRS Notice 2014-21 — US crypto tax treatment